The Yield Bubble & Inflation

The Yield Bubble & Inflation

20 Years in the making.

The Next Big Short

Let’s start at the end and work backwards. $TLT is a 20+ year U.S. treasury bond ETF. The weighted average maturity of the bonds is 26.1 years.

For the purpose of simplification and abstraction, we will assume the weighted average to be 25 years. When I refer to the bond yields, unless explicitly stated which one, I am talking about an equally weighted average of the 20 yr and 30 yr bonds.

At this point you’re probably thinking: “ok…. and?”

The Yield Bubble

“In finance, the yield on a security is a measure of the ex-ante return to a holder of the security. It is a measure applied to common stocks, preferred stocks, convertible stocks and bonds, fixed income instruments, including bonds, including government bonds and corporate bonds, notes and annuities.” (Wikipedia).

The yield of an investment is of the utmost importance to investors. For the layman, yield can be understood as: the expected yearly return of an asset, not through price appreciation, but underlying value increase.

If an investment does not have a good expected yield then it is not a good investment. So this means that a higher yield investment is better…..right? Not always. This is because a very high yield suggests way higher risk.

There are two big sections of the financial markets. Stocks and bonds. Stocks have yields just like bonds do. Stock yields are generally measured through earnings. The P/E ratio, while not the best yield ratio for value investors, is a good overall indicator of the price of a stock. A $100 stock with a P/E ratio of 10, makes $10 in earnings every year. Bonds work similarly, except their yield is determined by interest not earnings.

Imagine two nearly identical assets, we’ll call them asset 1 and asset 2.

- Asset 1 has a price of $100 & a yield of $100/year….that would mean it has a yield of 100%.

- Asset 2 also has a price of $100, but it only yields $40/year…meaning a 40% yield.

Why are the yields so different? It’s because asset #1 is more risky than asset #2.

The higher yield of asset 1 acts to incentivize investors for that higher risk. If you invest in asset 1, there’s a higher likelihood of losing money than with asset 2. But if the investment actually performs, your gains are way larger.

Generally, the goal is to outperform the major benchmarks. In the USA, the S&P 500 or Nasdaq-100 are generally used as a benchmark.

Yield tends to decrease as price increases. A stock can increase it’s yield by earning more money. A 10% yield before an earnings report can move to 20% without the price moving at all.

Bonds are different. Bonds do not have the ability to adjust the yield this way. Bonds have fixed interest rates. So the yield is entirely based on the price of the bond. A bond trading at $100 with a 5% interest rate has a 5% yield. If the bond sells off down to $50 then the yield increases to 10%.

Stock and bond yields act as a sort of yin and yang that balance each other out. If $100 total dollars are in a market and there is a stock with $50, with a yield of 10%, and a bond with $50, with a yield of 2%, there would be a skew towards the stock.

This would cause stock price to go up and yield to go down. Let’s say the new price is now $90 and the yield is now 5.5%. However since there is only $100 dollars in the market the bond must be worth $10, which would now give it a yield of 10%.

Now the bond seems like the better investment and investors would rotate back into bonds.

This cycle is never ending. Until now.

This is a list of the current treasury bond yields.

30 yr ---- 1.89%

20 yr ---- 1.86%.

10 yr ---- 1.46%.

5 yr ---- 1.09%.

These extremely low yields must mean stocks are cheap compared to their earnings, and that stock P/E’s should be near historical lows. The historical average P/E is 13 to 15. But the current P/E of the Nasdaq-100 is 36.86. An earnings yield of 3.7%.

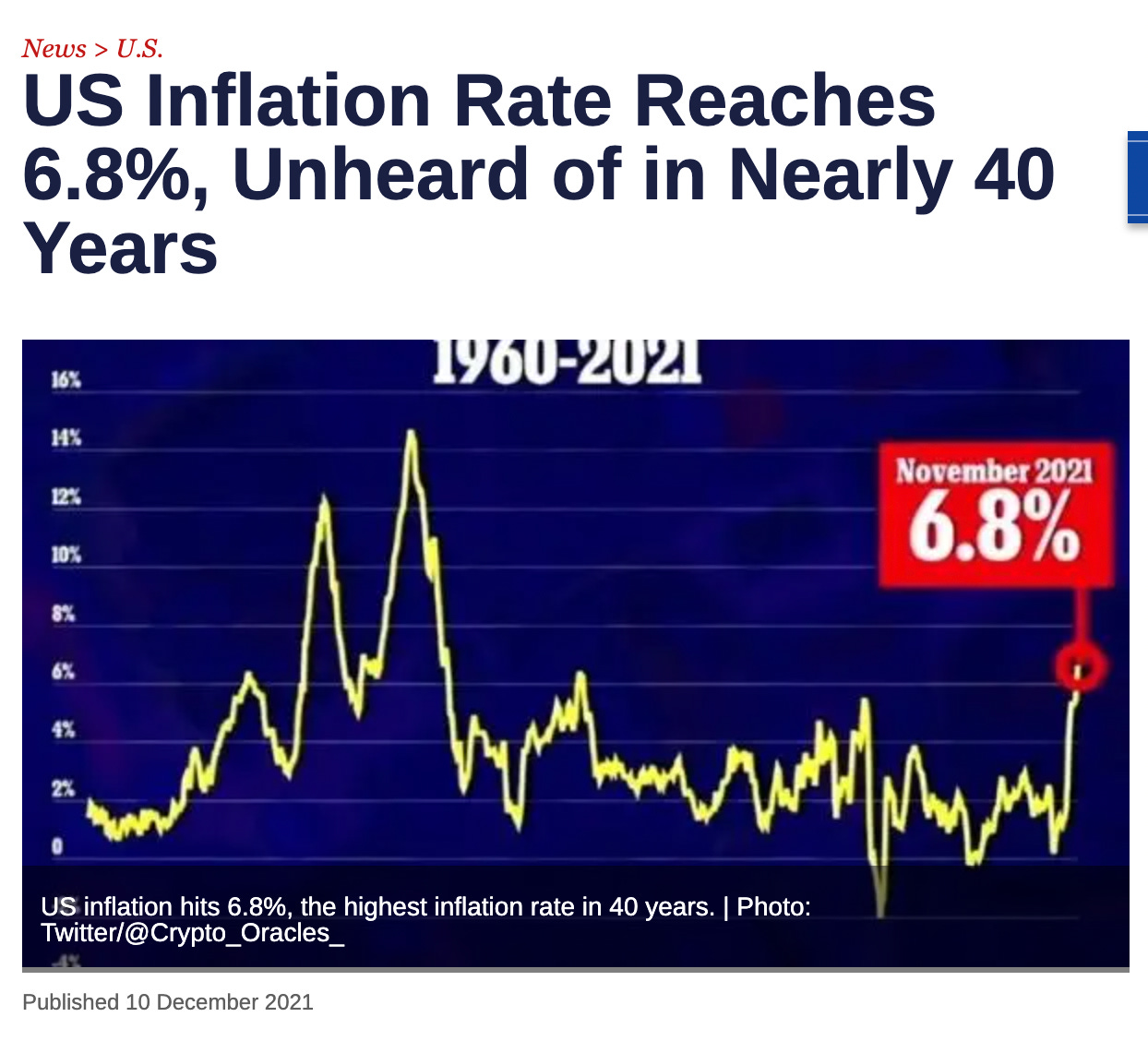

Inflation is at 5.4% in 2021. This means for any investment you make right now, whether it’s a stock or a bond, you would need it to yield > 5.4% in order to outpace inflation. But as mentioned earlier, bond yields are < 2.0 %, and stocks yields are 3.7%

Now for some quick math:

30yr bond yield (1.89%) - Inflation (5.4%) = - 3.51%

S&P 500 stock yield (3.7%) - Inflation (5.4%) = -1.7%

This means if you were to invest in the market right now, both stocks and bonds would give you a negative real yield.

The average inflation rate since 1983 has been about 2.85%. This intentionally excludes the inflation of the 70s and early 80s to show a more normalized average. The point here is to illustrate that even with a more normal rate of inflation, the net earnings yield we’d expect to see for bonds @ current interest rates & the NASDAQ @ current P/E ratios would still be negative & ~ 0.9% respectively.

Why do people in top institutions and individuals alike continue to buy these securities? What are we missing here?

Speculation, expectation and denial

“Those Aren’t Eating Sardines, Those Are Trading Sardines!”

In a book titled, “Margin of Safety” Seth Klarman describes a story about sardine merchants who, upon a shortage of sardines, began to hoard sardines and bid them up to absurd prices only on the premise that someone else would pay more for them. Eventually, someone unfamiliar buys a can and eats the sardine and says “These sardines taste horrible!” to which the merchant replies “Those aren't eating sardines, those are trading sardines!”. The idea that something has no value to the owner other than what someone else is willing to pay for the item is absurd. There is an underlying value to securities and even more tangible things like farmland. This underlying value is delivered through the yield. So why do bond holders keep holding their bonds if they are effectively liabilities to the holder? The answer is that the bonds aren’t yield bonds, there are trading bonds!

Again from The Margin of Safety,

“For still another example of speculation on Wall Street, consider the U.S. government bond market in which traders buy and sell billions of dollars' worth of thirty-year U.S. Treasury bonds every day. Even long-term investors seldom hold thirty-year government bonds to maturity. According to Albert Wojnilower, the average holding period of U.S. Treasury bonds with maturities of ten years or more is only twenty days.”

Bonds have effectively become hot potatoes passed on from one trader to another.

But why accept it if it is still a liability, even on a normalized inflation scale? Someone must be buying these things at a rate that would give traders a reason to continue to speculate on them? Who would be so unwise as to accept these things? It’s obvious….The United States Federal Reserve

We Print Digitally

Since June 2020, the Fed has been buying $80 billion of Treasury securities and $40 billion of agency mortgage-backed securities (MBS) each month. This is known as quantitative easing or “QE”.

QE exists to prop up asset prices. The Fed prints digital money, then uses that money to buy us treasury bonds from banks. This has the effect of increasing the available money banks have for loans, without increasing their total liabilities or debts.

The banks don’t actually spend that money, they simply hold it in internal ledgers. With extra money in their ledger, banks can then offer low interest rate loans for people & businesses to finance new purchases or raise capital. This “juices” the economy as it causes an overall effect of increased spending.

What if Inflation starts to get out of control?

If people start to think a dollar is worth more now than it will be in the near future, they will make every effort to buy things they need NOW instead of waiting for lower prices. If everyone starts doing this, the belief of impending inflation becomes self fulfilling.

This is why the white house and federal reserve are terrified to acknowledge inflation. They will deny deny deny, even in the face of credible signs that inflation might get serious. If rapid inflation does becomes an issue, what is something that can be bet against? Something with a yield that correlates with inflation?

$TLT

The single best trade in this scenario is to short bond prices or go long bond yields. Buying put options on $TLT bond prices is the best route. Options allow the investor to leverage their buying power for the trade off of added risk in the form of limited time. '

| Seeking Alpha")

Timing is important in options, but it’s impossible to predict short term price movements in the market….. which is why a 2-3 year out put option is the best choice. It allows for the most leeway in timing at the cost of smaller expected returns.

Without overly complicating option pricing, Implied Volatility (IV) can be looked at as the price of the option. IV is the expected volatility of the option, or how much the person on the other side of the trade thinks the price will fluctuate over the course of the option.

This is a key issue with the Black-Scholes model, the model that is used to price options. It is almost impossible to be able to predict the rate of price appreciation or depreciation over a 27 month period.

The IV on the $115 strike 2024 TLT put options is 21.5%. That means the option seller believes that TLT will trade in the ranges of 118.5--183.5. 118.5 would imply a bond yield of 3.2% from 1.875%.

Remember, inflation is currently 5.4% for 2021, with an average rate of ~2.85%. In order to profit, TLT would have to go from today’s price of $151 to $110 by 1/31/2024.

Price - return %

100 = 237%

95 = 349%

90 = 462%

75 = 799%

$75 would imply bond yields to go to about 5.6%. This isn’t unreasonable.

Keep in mind these are gains on the date of expiry, if the sell off in bonds happens earlier, the options are worth even more.

If the bond market becomes volatile, the IV on the option skyrockets; making it worth more.

There are risks to this trade idea. The Fed could revert their decision and continue to print money and continue QE, pushing the pop out further. Foreign buyers could swoop in on the U.S. treasuries. These two events would likely be short lived, courtesy of inflation.

Disclaimer

These are solely my thoughts, and are not intended to represent professional guidance or advice on how to invest your hard-earned money. I like to lay out my thought process for certain investments on my website as a way to receive genuine feedback & input.

You should always do your own research & think twice before following in the footsteps of a random blogger such as myself. I’d also like to emphasize that I am NOT a professional, and am simply an amateur investor.

Cheers,

-yonathan.