Ingles Markets

Ingles Markets

Significantly undervalued $1 billion recession-resistant business

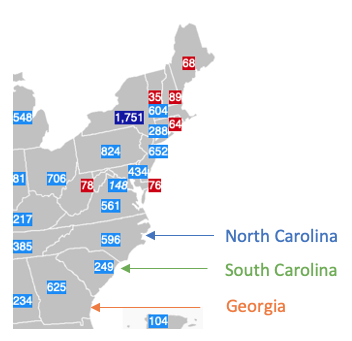

Established in 1963, Ingles Markets is a leading supermarket chain in the Southeast, operating 200 supermarkets in North Carolina, Georgia , South Carolina, Tennessee, Virginia and Alabama. All their supermarkets operate in suburban areas and small towns, limiting inroads of other chains and potential competition from entering and taking away from their market share. Many of the locations are often in the last populated areas before becoming very remote (Like at the base of mountains, rural Appalachia etc.).

Stores include food, pharmacy, general merchandise, and gasoline. Real estate holdings are considerable and include about two thirds of their stores. Ingles is staffed by 27,000 non-union employees. They also own their own dairy which produces 60,000,000 gallons annually and supplies Ingles Market and others. All of these are extremely attractive selling points in the medium-term, and the risk-reward is very favorable.

Thesis

Significantly undervalued $1 billion market cap recession-resistant business

The pandemic has generated greater than 25% FCF yield and has resulted in a doubling of profits

Quietly paid down over ¼ of a billion in debt last year (from $840M to $586M)

Should continue gushing elevated cash flows for the time being

With no plans for expansion, predictable Cap Ex, low dividends due to corporate policy and FCF that will significantly exceed further worthwhile debt reduction, IMKTA will have no other rationale choice but to use excess cash to buy back more shares than they already have.

Over 10% of the float has been sold short and this combination has the potential to drive up share prices

Added protection comes from an undervalued real estate portfolio

A shy company with no earnings call waiting to be discovered by others (Michael Burry & Mario Gabelli are major shareholders.

The Pandemic Has Catapulted Margins and Income

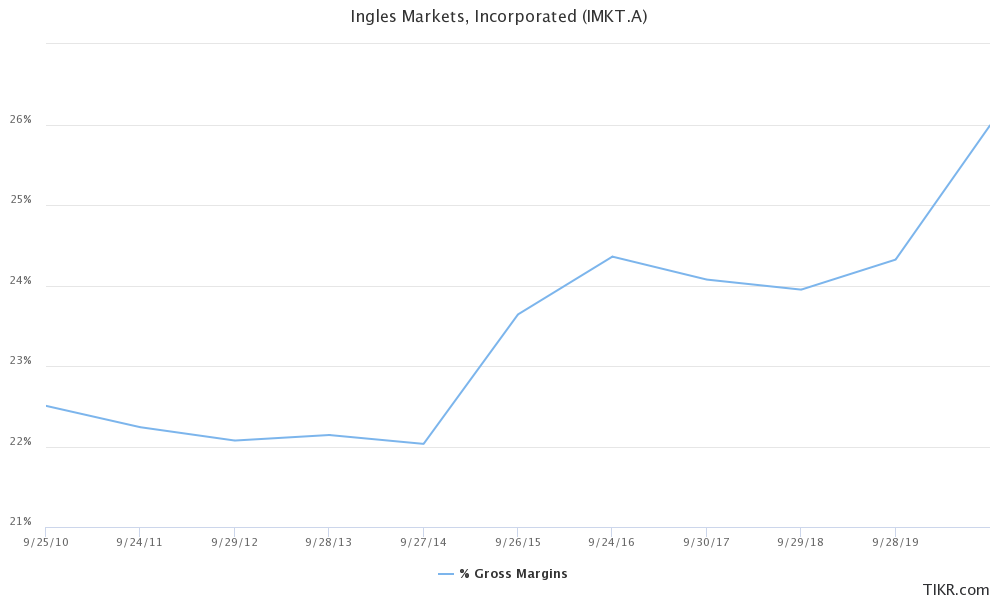

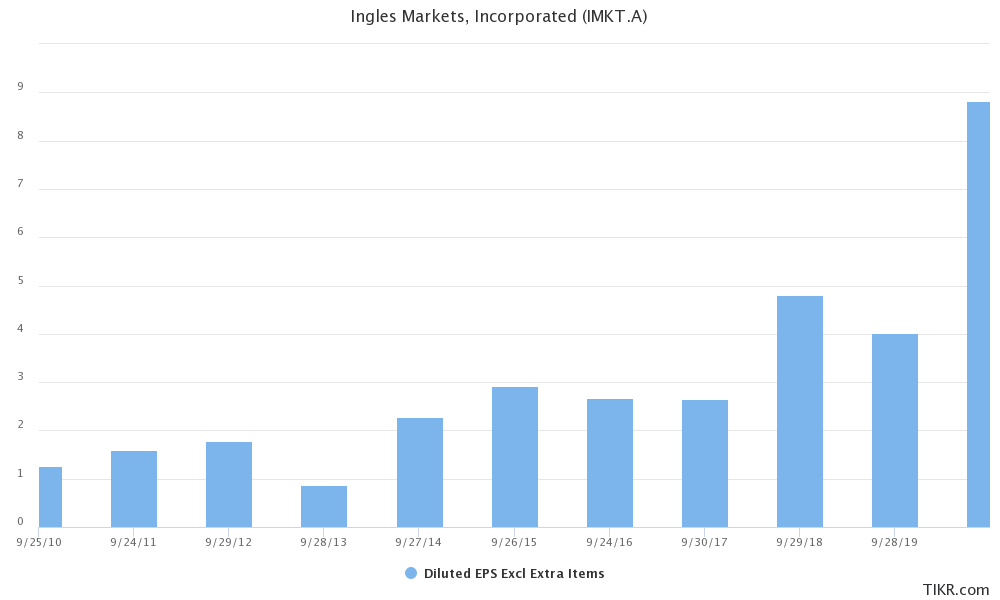

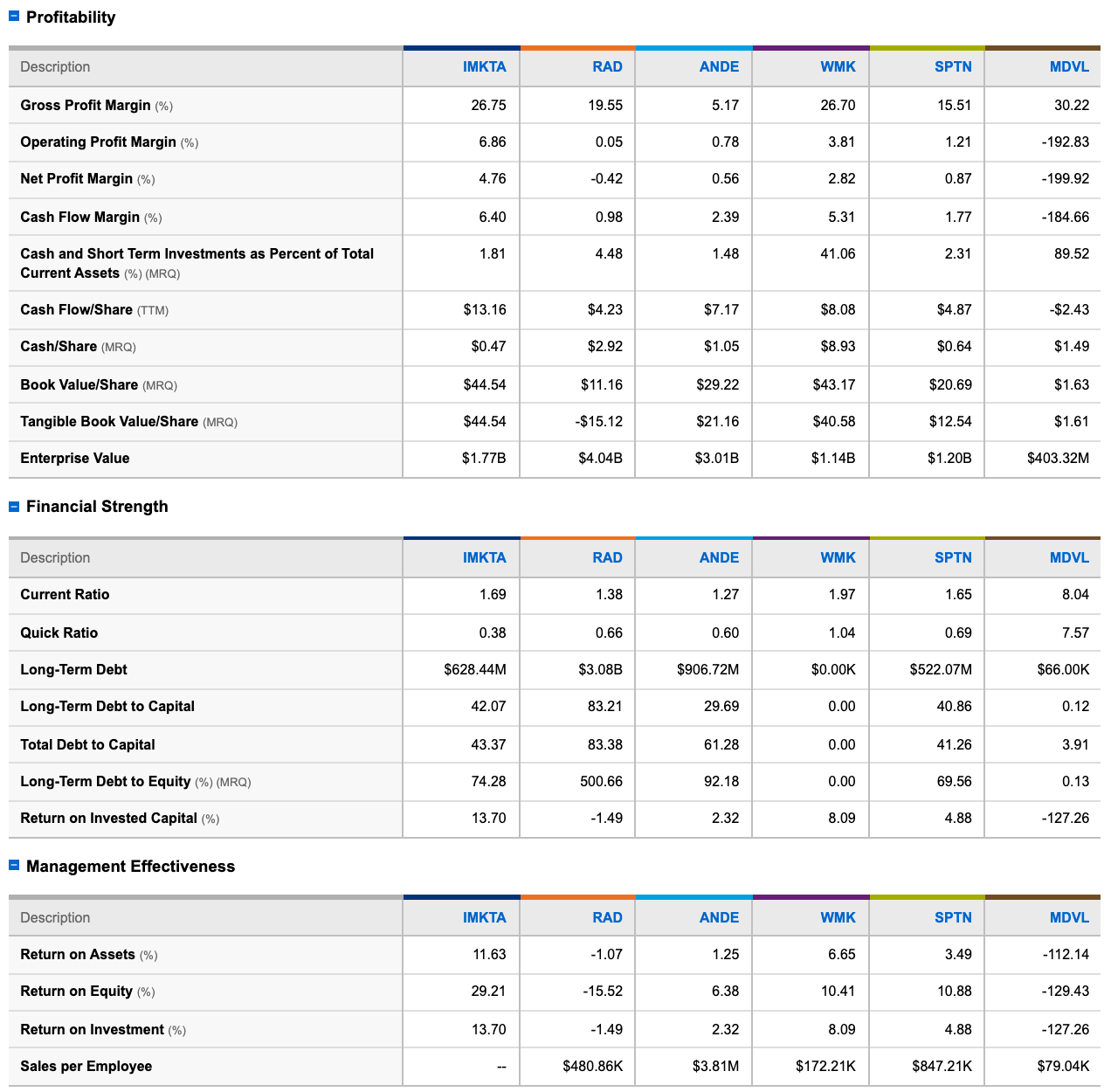

IMKTA has been a cheap company for a while (see upcoming competitors comparison table). Pandemic behavior changes have more than doubled profits by increasing sales but mainly by increasing margins. Retail comparable sales excluding gasoline increased 15.1% during fiscal 2020 compared with 2019. The number of transactions (excluding gasoline) decreased 3.1% while the average transaction size (excluding gasoline) increased by 15.8%. Comparing fiscal 2020 with 2019, gasoline gallons sold decreased 6.3% and per gallon gasoline prices decreased 15.6%.

These temporarily higher margins have translated to stunning increases in profits. Their TTM EPS is $10.61 while their stock price is just over $60 per share so they have a trailing TTM PE of ~5Xs. However, their MRQ margin remains elevated and could remain so for perhaps another year.

Their margin opportunity outside of the pandemic relates to private label products which they are promoting so far with what appears to be limited success.

They also could benefit from further vaccine distribution into rural areas. Currently, the shingles and flu vaccines are very popular but they have not received the Covid-19 vaccine and its not clear how large the impact will be. Most pharmacies have struggled during the Pandemic with more online pharmacy sales but vaccines must be done in person and can drive profits and margins and people into the stores.

Improved gas sales are likely with the economy reopening.

The Two Company Share Classes Have Caused Dividends To Be Abnormally Low

There are two share classes: A & B. The Bs are not publicly traded and are owned by the founding family and have 10 votes per share. The Bs are convertible to As on a 1 for 1 basis. The COB owns 29% of the company but has over 75% of the voting rights.

However, the As do a have a small advantage in that they are guaranteed a 10% premium on dividends compared with the Bs. Consequently, Ingles pays a pathetically small dividend. Last year they paid out 9% of earnings as dividends. My guess is this premium has caused Ingles to keep the dividend abnormally low.

They pay out about $13 million a year in dividends.

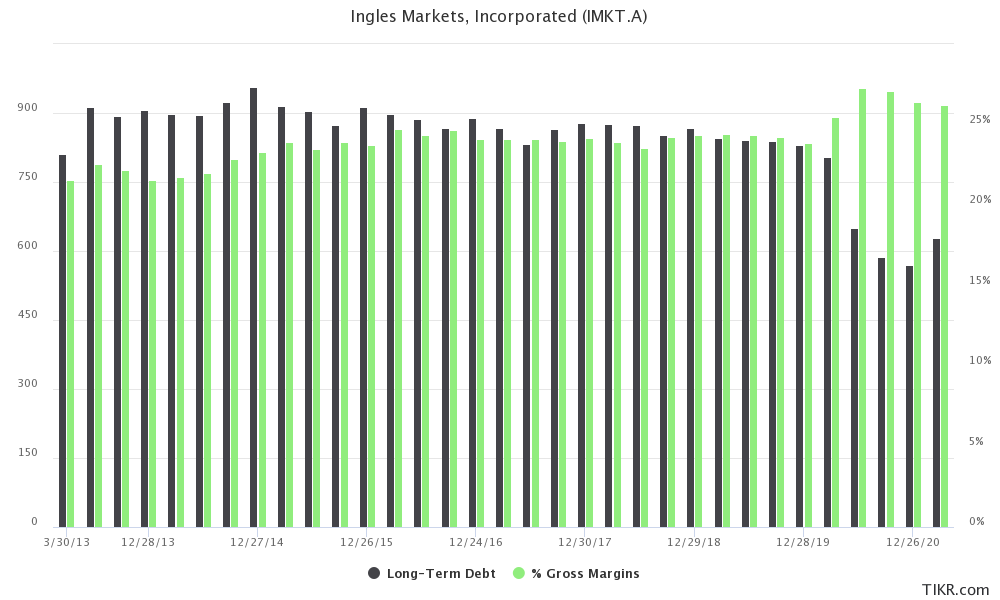

Company Debt Has Fallen Dramatically And The Trend Should Continue Due To Excess FCF

FCF went from $50M (2019) to $230M (2020). Last year their staggering windfall profits primarily went to pay down debt. A $1 billion market cap company paid down over ¼ billion in debt in twelve months!

In 2019 (FY) they paid $47 million in interest. In the quarter ending Dec 20, 2020, they paid $6 million. Their highest interest rate debt comes due in 2023 and costs approximately $17 million per year.

The Senior notes which mature in 2023 have an interest rate of 5.75% have been paid down from $700 million in 2019 to $295 million in 2020. This year they will be able to call these notes at par effectively lowering the cost of paying off this debt early………..and last eek they did exactly that. IMKTA announced the refinancing of the 5.75% notes and bank loans with new 10 year 4% notes. In their sec filing last Wed, they indicated that after the issuance they would have about 609mm in debt outstanding. I just checked the 10-q and debt outstanding at q end was bouut 40mm higher annual savings on the new debt should be a little over 5mm or about 25 cents a share.

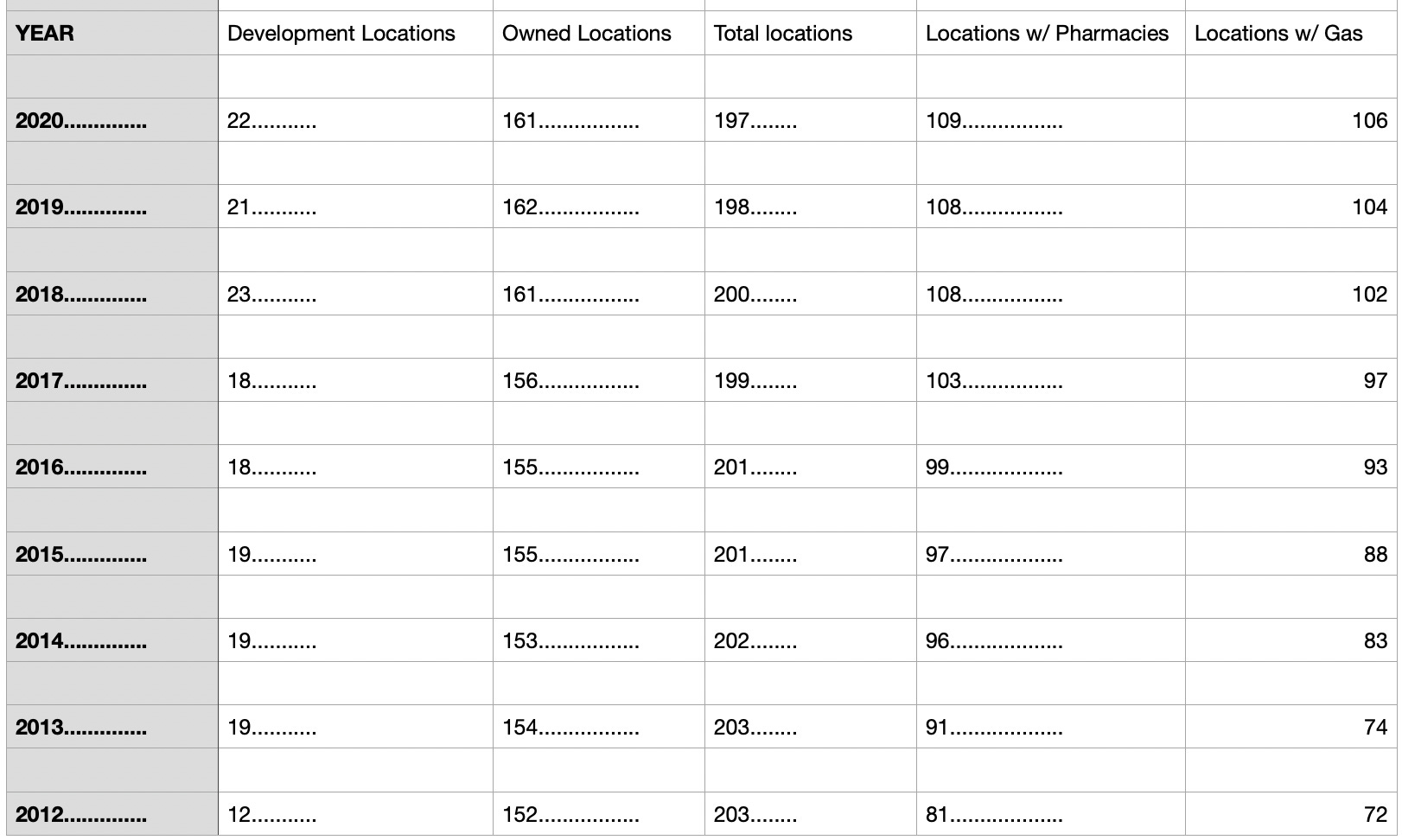

The following table shows how they expanded since their last refinancing in 2013.

Over the past 8 years management increased development locations from 12 to 22 ,owned locations from 152 to 161 , meanwhile total locations fell slightly. In store pharmacies went from 81 to 109 and fuel locations jumped from 72 to 106.

If we assume that management will maintain the same pace of owned store locations (about 1 a year) and that most fuel and pharma locations have already been built (notable slowdown in past 3 years) the expenditures for plant and equipment shouldn't be more than the recent past. Cash flows on the other hand should be much higher with the payoff of debt last year and the current refinancing.

(annual)

(quarterly)

FCF was $266 million in TTM. Their margins remain high and they will pay less in interest by $25+ million annually going forward. Their dividends are limited and the most current 10-q shows interest expense dropping to 6.2mm from 12mm same quarter 2019 or 5.8 mm in quarterly savings or about 23mm a year add another 5mm form last weeks refinancing and you get about 28mm in annual savings or just under 1.50 a share.

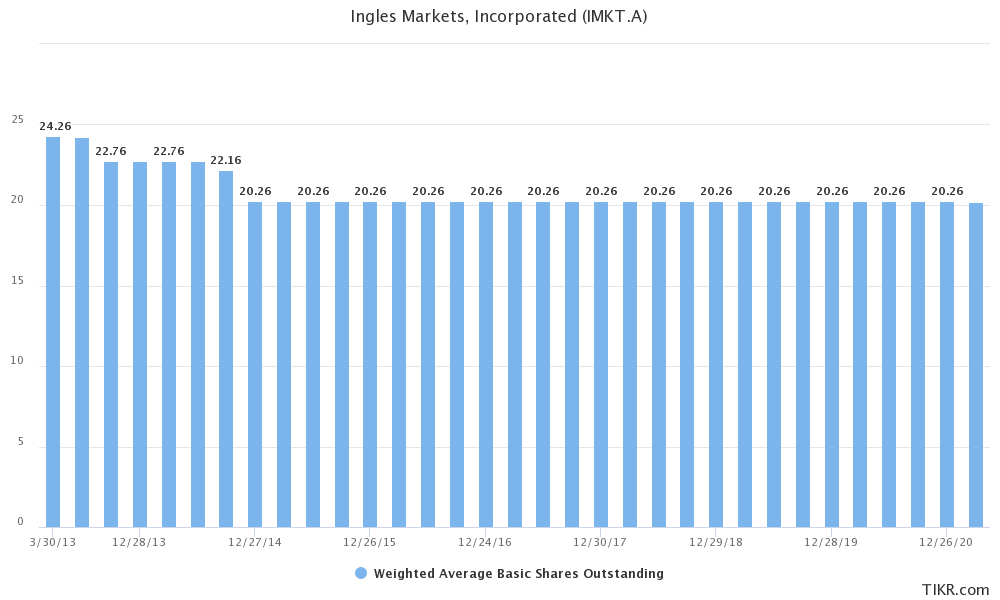

B/c they lack significant growth plans they really have 1 choice left on what to do this year with all this massive cash flow: Buy back shares.

Since FCF Significantly Exceeds Potential Debt Reduction, It Is Logical To Anticipate Share Buybacks. There has been no change in the share count since 2015 which is right before James Lanning became CEO when Robert Ingle, controlling shareholder, relinquished the job but retained the Chairman of the Board role. The company doesn’t award stock options. They straight up have too much money.

The last time they announced the refinancing the stock was up about 30% in about 6 weeks. If we move to 13x $6.00 normalized earnings we should go to 78 or about a 20% move. Michael Burry’s Scion Asset Management bought 111,415 shares in Q4-2020. He has agitated for management to buy back shares in some of his past plays and this one seems to fit that theme perfectly.

The Short Interest is 10% of the float. It’s not hard to imagine how an additional stock buy back will be received by the market in a company that Michael Burry is invested in after the GameStop craziness.

To be clear, management has not indicated they will buy back more shares, but they barely indicate anything. They have not had an earnings call since the new CEO took over 5 years ago, and when I emailed them with a bunch of questions, they ignored me & mailed this packet with their 2020 financials.

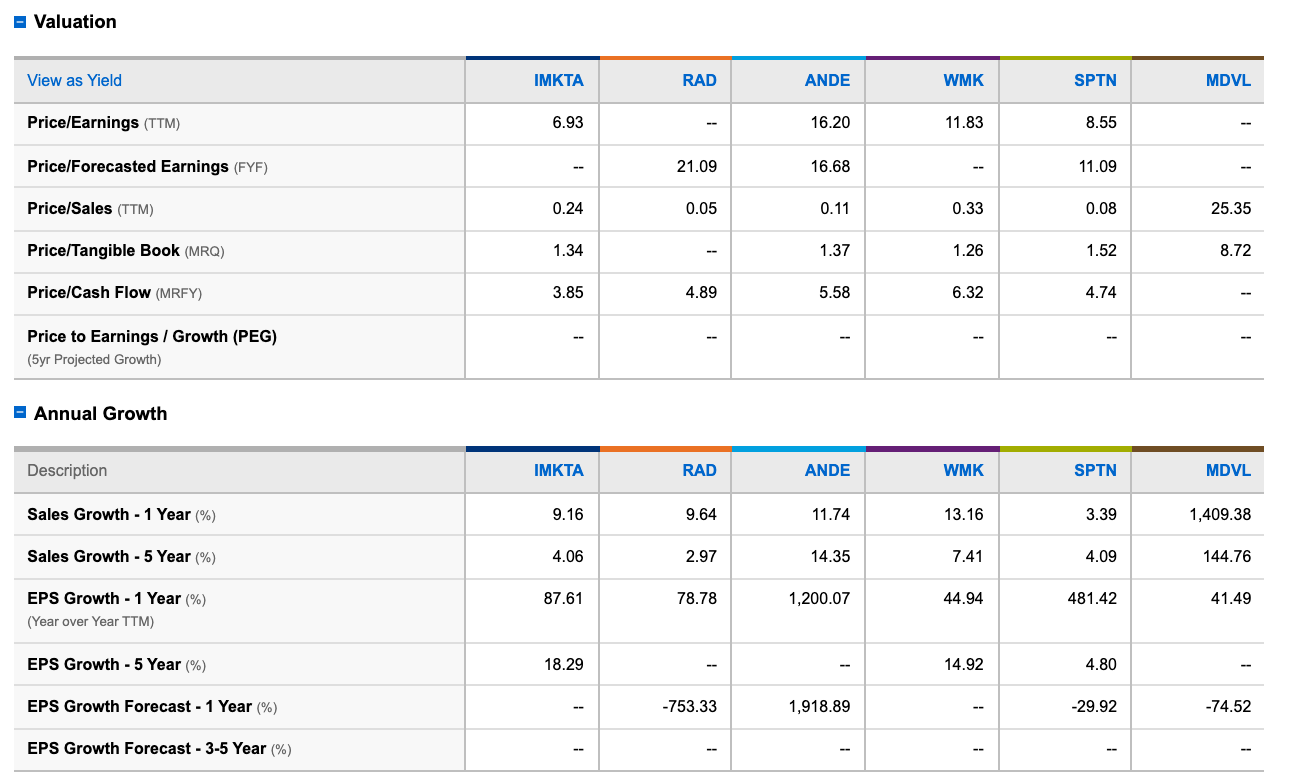

Current IMKTA Valuations Are Attractive

Their industry is a recession resistant one and Ingles valuations are very favorable compared with their competitors.

A unique aspect of Ingles is their real estate portfolio. They have long held significant real estate that is held at book and worth substantially more than $1.1 billion reported. Out of the 200 supermarkets, Ingles owns 162 outright as either free-standing stores or the anchor tenant in an owned shopping center. This implies significant real estate value and makes the company attractive from an outside view given its hidden asset value. The company also owns 21 undeveloped sites suitable for a free-standing store or development by the company or a third party.

How much is the portfolio understated? Real estate in North Carolina, South Carolina and George has appreciated over the years. The stated book value of the real estate is $37.71 per share, meaning the stock is trading at just 1.32 price-to-book. These unencumbered real estate assets, along with the significant debt repayment, give the company flexibility in the future.

Other positives include over funded self-insurance which could have excess funds over debt of $45 million.

Risks

· Online grocery delivery

· Weather

· Competition

· Rent collection issues

· Potential rising labor costs

· COB has >75% of voting rights

Catalyst

· Stock buyback

· Potential short squeeze

· Margins remain elevated longer

· Vaccine distribution

Disclaimer: I and/or others I advise hold a material investment in the issuer's securities.

***This is not financial advice because I don’t know anything. In fact, you’re probably better off inversing my plays.