GameStop’s Metamorphosis

Why the World’s Most Infamous Meme Stock is Now a $9 Billion Optionality Play

Executive summary

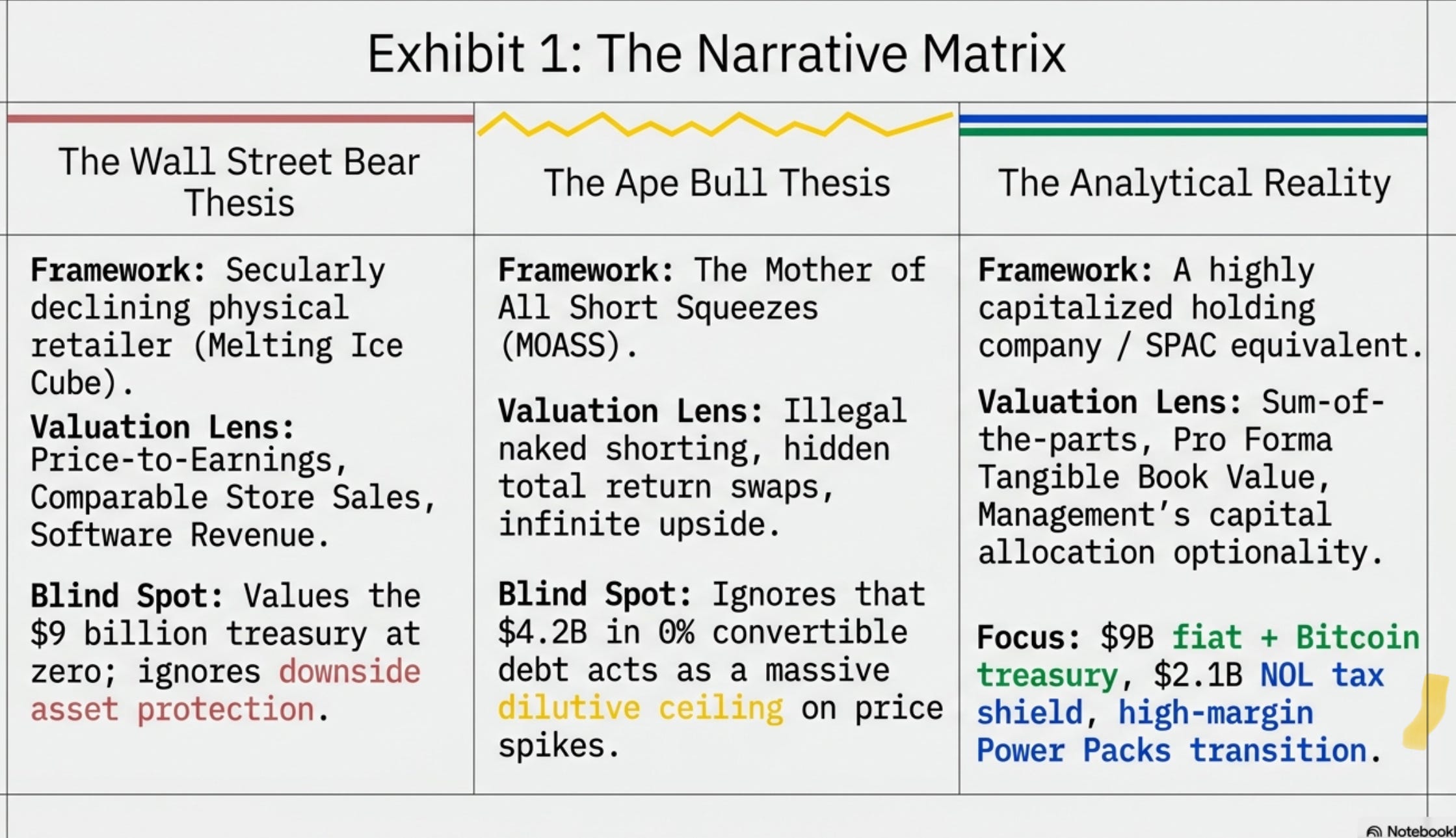

The evidence overwhelmingly indicates that GameStop GME 0.00%↑ is no longer accurately defined as a retailer. Instead, the company is best understood today as a highly capitalized holding company and cash-rich optionality play, supported by a structurally declining but ruthlessly optimized retail business that serves primarily to preserve valuable tax assets.

GameStop operates with profound asymmetrical advantages that confound traditional valuation frameworks. Through a series of highly disciplined at-the-market (ATM) equity offerings during periods of extreme market volatility, aggressive zero-coupon convertible debt issuances, and strict cost rationalization, the company has accumulated a fortress balance sheet. As of the end of fiscal year 2025, GameStop commands $9.014 billion in liquid fiat assets alongside $368.4 million in Bitcoin holdings. Concurrently, its physical footprint has been aggressively pruned, with the United States store base shrinking from 2,915 locations in early 2024 to 1,598 stores by January 2026.

The underlying operating business has intentionally pivoted away from low-margin hardware and physical software toward a higher-margin collectibles segment, which now accounts for nearly thirty percent of total revenue and has driven the company back to GAAP profitability.

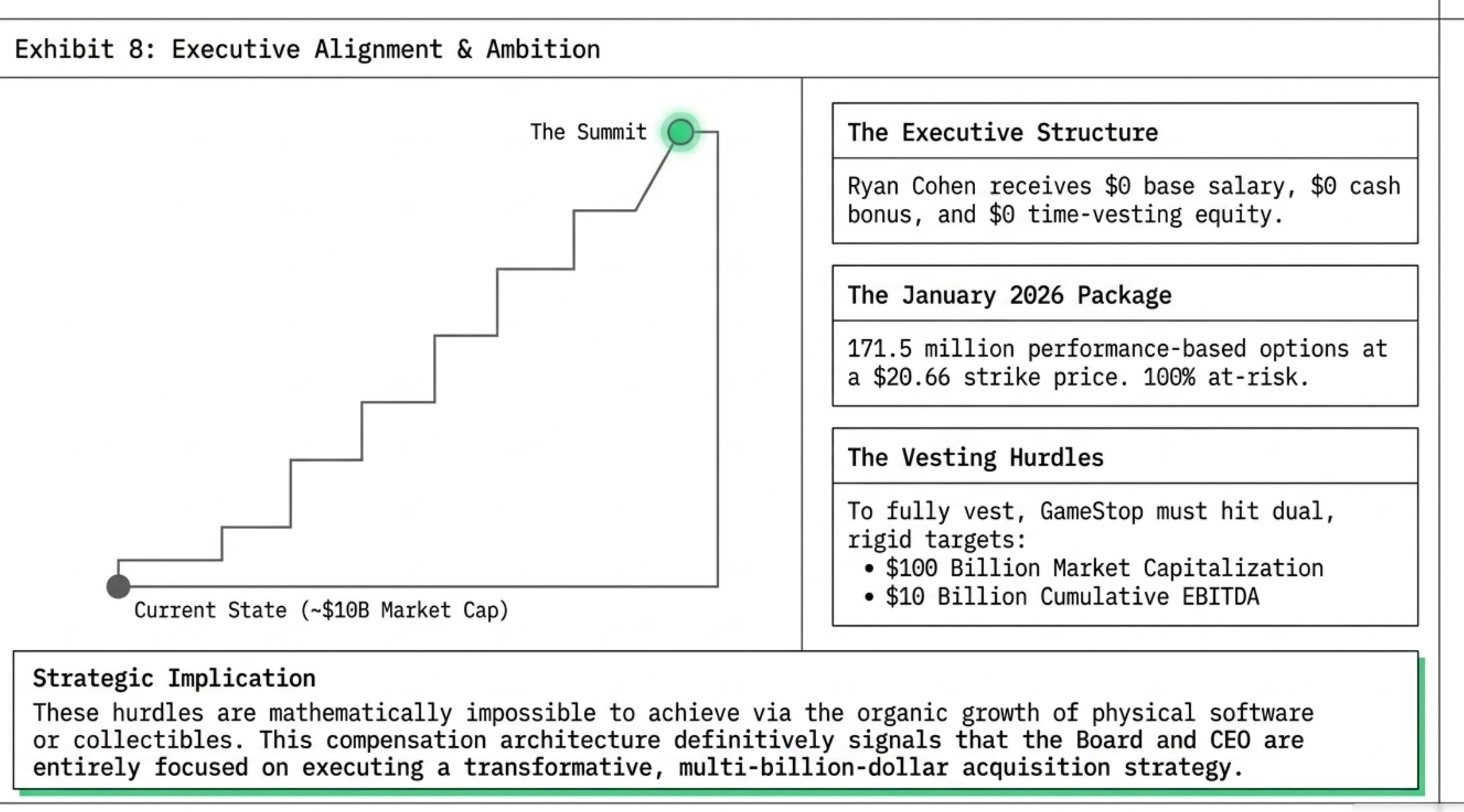

The current market capitalization hovers between $10.3 billion and $11.0 billion. When backing out the vast cash reserves and the face value of the zero-interest debt, the implied enterprise value of the legacy operating business approaches a liquidation floor, trading at a marginal premium to the company’s pro-forma tangible book value. The strategic direction of the firm is explicitly telegraphed by the compensation structure of its Chairman and Chief Executive Officer, Ryan Cohen. Cohen receives no salary, no cash bonus, and no time-vesting equity. Instead, his compensation is tied entirely to a recently approved options package requiring GameStop to reach a $100 billion market capitalization and $10 billion in cumulative EBITDA to fully vest.

These targets are mathematically impossible to achieve via the organic growth of the legacy retail operations, signaling definitively that GameStop’s ultimate trajectory relies on executing a transformative, conglomerate-style acquisition strategy.

Takeaway 1: It’s Not a Retailer, It’s a $9 Billion Treasury

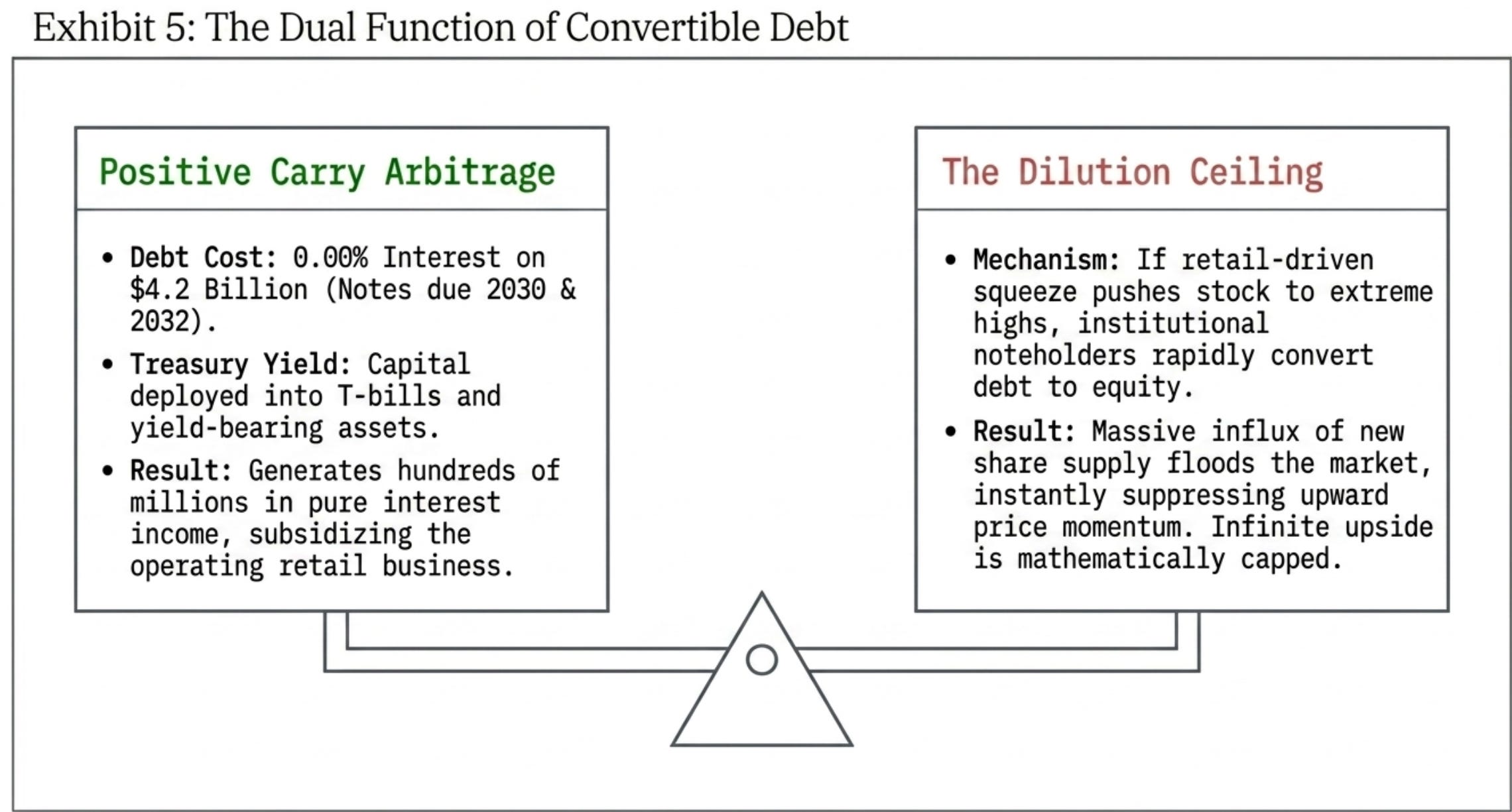

The most critical fact for investors to grasp is that GameStop is no longer a retail business; it is a hedge fund with a retail side-hustle. As of the end of fiscal year 2025, the company commands a massive liquidity position: $9.014 billion in fiat assets and a strategic reserve of 4,710 Bitcoin (valued at $368.4 million). While the treasury has expanded, the retail footprint has been ruthlessly pruned. From 2,915 U.S. stores in early 2024, the count has plummeted to 1,598 by January 2026. However, the business is not just shrinking; it is optimizing. By pivoting toward a high-margin “Collectibles” segment—which generated $1.060 billion in 2025 (nearly 30% of revenue)—and launching the “Power Packs” trading card platform in April 2026, GameStop returned to GAAP profitability with $ 418.4 million in net income . Crucially, GameStop has performed a sophisticated arbitrage by issuing $4.2 billion in zero-coupon convertible senior notes. By raising capital at 0.00% interest and deploying it into yield-bearing Treasury bills, the company generates hundreds of millions in risk-free interest income, essentially creating a positive-carry situation that subsidizes the “melting ice cube” of retail.

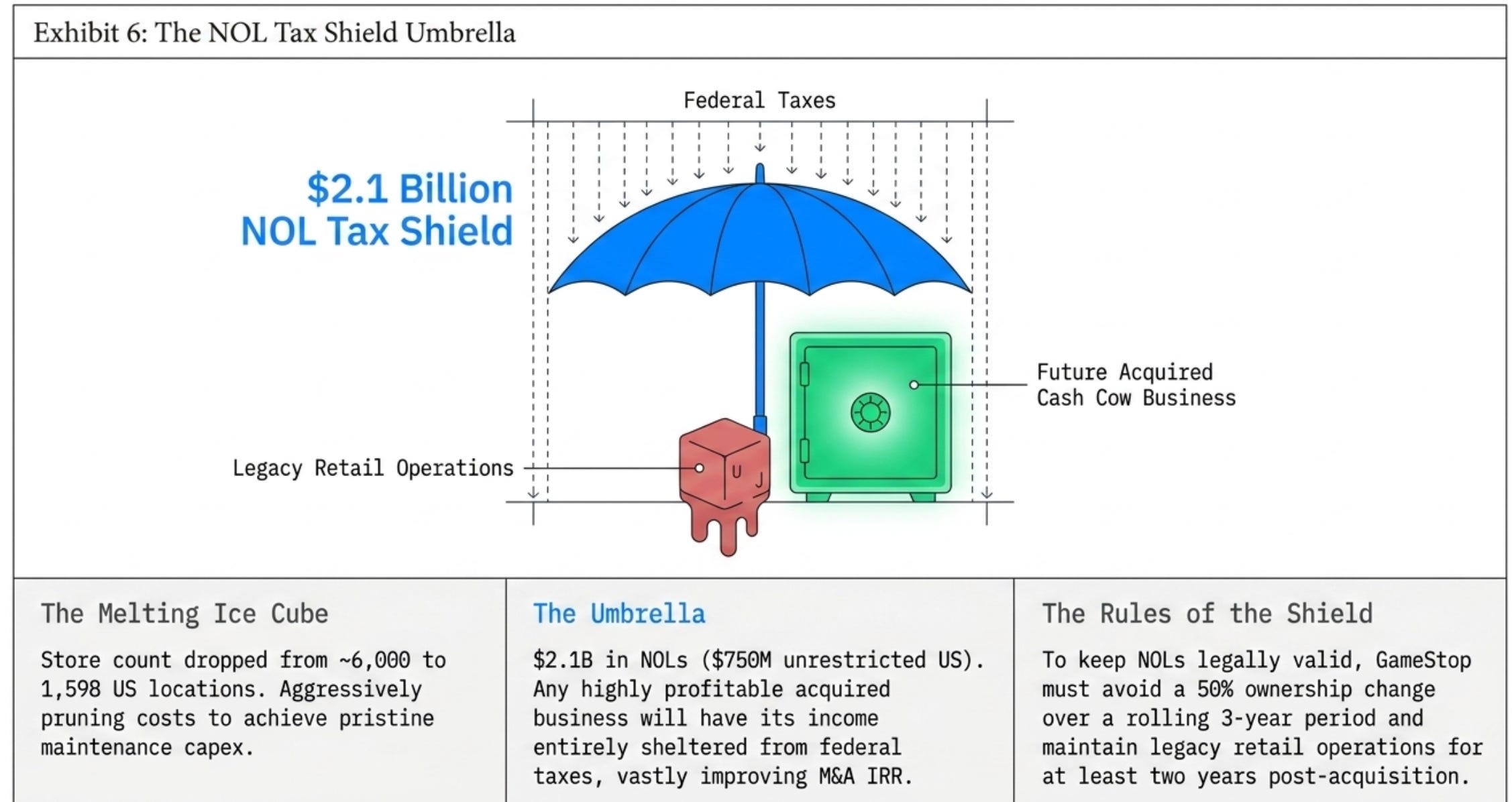

Takeaway 2: The $2.1 Billion “Secret Weapon” Tax Shield

Hidden within the balance sheet is a $2.1 billion Net Operating Loss (NOL) asset. A look at the filings reveals the “secret weapon” is actually ~$ 750 million in unrestricted U.S. NOLs, which can be used to shelter future income from federal taxes. This creates a specific strategic constraint for CEO Ryan Cohen. Under Section 382 tax laws, a “50% ownership change” within a rolling three-year period would significantly limit these benefits. This explains why equity offerings have been carefully spaced out. Furthermore, Cohen likely cannot shut down the legacy retail operations entirely; the “old business” must remain active for at least two years post-acquisition to keep the NOLs alive. The retail stores are no longer the engine—they are the shield.

Takeaway 3: The “Moonshot or Nothing” CEO Pay Package

In January 2026, the board approved a compensation architecture for Ryan Cohen that serves as a definitive strategic signal. Cohen receives no salary and no cash bonuses. Instead, he was granted 171.5 million stock options with a $20.66 strike price. This award is “100% at-risk,” meaning Cohen only profits if he maintains the current price floor while hitting staggering milestones:

A market capitalization scaling to $100 billion .

$10 billion in cumulative EBITDA.Since these targets are mathematically impossible to achieve via 1,500 video game stores, the package confirms that GameStop’s path forward relies on a transformative, conglomerate-style acquisition strategy. Cohen is incentivized to swing for the fences with his $9 billion war chest.

Takeaway 4: The Warrant Trap—Monetizing the “Meme” Automatically

GameStop has pre-positioned itself to monetize future volatility through an “ingenious trap.” In October 2025, the company distributed a warrant dividend with a $32 strike price . This is a masterstroke for handling “meme-stock” surges. By using these warrants, the company can bypass the “friction of SEC filing delays” that typically occur during a short squeeze. If the stock crosses $32, the company raises $ 1.9 billion automatically with “no volume restrictions” and “zero trading slippage.” It is a mechanical system to turn volatility into cold, hard cash.

Takeaway 5: Buying the “Buffett of 1969” for Free

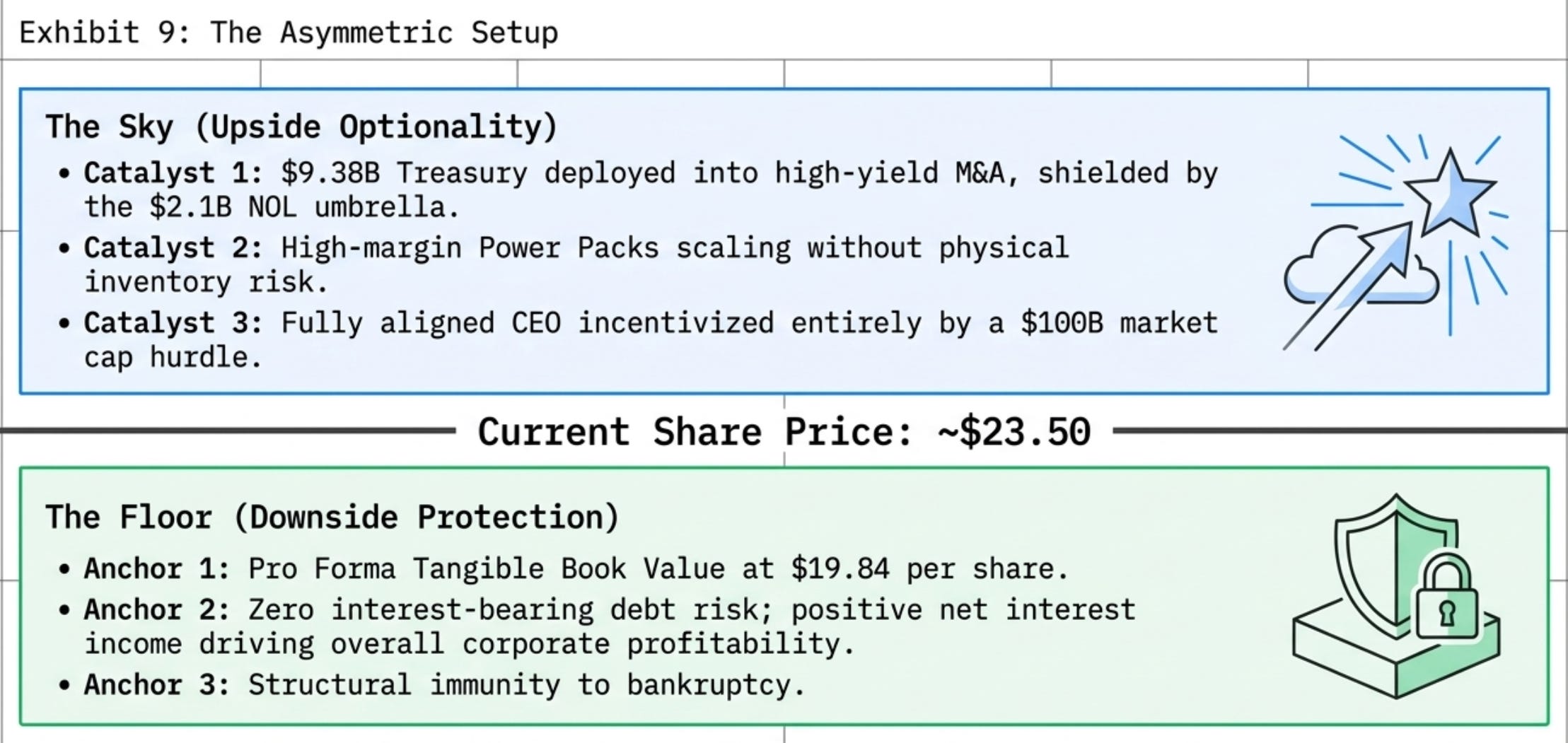

At a current share price of roughly $23.50, GameStop trades at just 1.18x its Pro Forma Tangible Book Value (TBV) of $19.84. This valuation implies that the market is assigning almost zero value to the operating business, the brand, or the tax shield. The parallel here is Berkshire Hathaway in 1969. Much like Warren Buffett used a dying textile mill to generate the “investable float” required to purchase cash cows like GEICO, Cohen is using a shrinking retail footprint and a massive cash pile to fund a search for “growing, giant piles of cash.”

Conclusion: The Asymmetric Bet

The real story of GameStop is no longer about video games; it is an asymmetric play on capital allocation. The downside is protected by an impenetrable floor of $9 billion in cash and a $19.84 tangible book value, leaving the company with functionally zero risk of insolvency. The upside is a long-dated strategic option on what Cohen does with the “investable float.” For the potential investor, the question isn’t whether the mall is dying—it’s how much that $9 billion will be worth once it is deployed into a new, profitable engine of growth.