European Banks

European Banks

Ever since the GFC European and UK banks have suffered from consistently falling net interest margins. Falling rates were great for tech stocks, but awful for banks. It has been 10 years of pain, but the tide is turning and the valuation set up is one of the best ever.

Low interest rates in Europe have been a headwind for bank profitability, but another under appreciated headwind has been the heavy regulatory changes and increased capital requirements. Before the 2008 financial crisis, the minimum capital requirement for a large Tier 1 bank was 4% of risk weighted assets

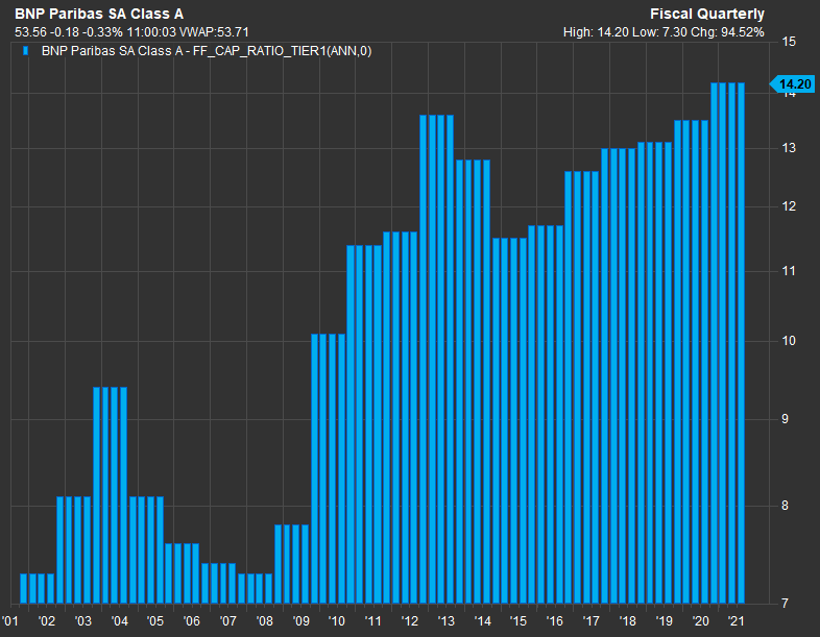

The 2008 financial crisis changed this, with regulators changing the minimum capital ratios from ~4% to ~ 14% for large banks. Below is the Tier 1 capital ratio for BNP Paribas. You can see it increased from 7% to 14%.

This multi-year upshift in tier 1 ratios from 7% to 14% was not easy, and practically nuked the stock valuations of all European banks. Why? Because in order to comply with the new regulations, they had to:

Issue new capital,

Stop growing or reduce assets,

Retain as much earnings as possible & deal with negative interest rates set by the ECB.

US banks got through this cycle quickly for a myriad of reasons that I don’t want to get into, but my main point is this: Economies grow when banks want to lend. But for the last 12 years, European banks haven’t been lending, they’ve been deleveraging and pacifying regulators who were angry at the banks for causing the ‘08 recession. While American banks got a slap on the wrist for causing the ‘08 crash, European bank were metaphorically in “jail”.

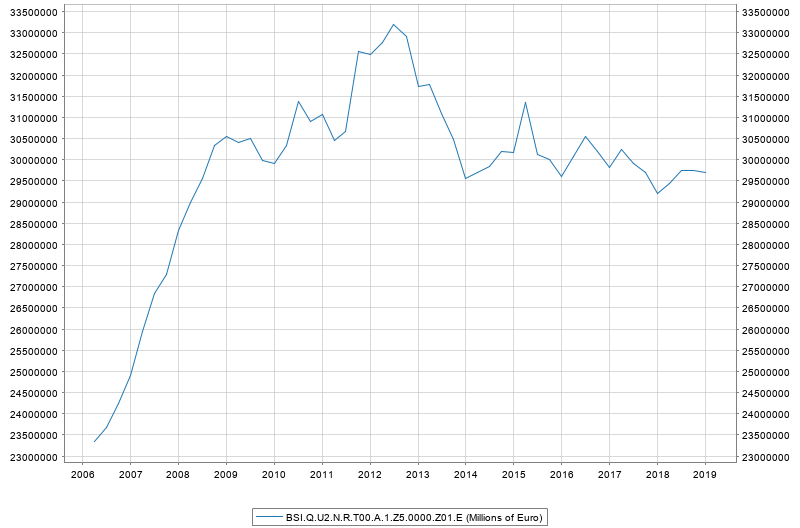

Europe is perceived as a low growth economy, but it’s rarely mentioned how outrageously low interest rates have largely disincentivized large banks from lending, and outright prevented smaller capitalized banks from lending as well. From 2009 to 2019 European banking sector assets were flat at EUR 29.5 trillion.

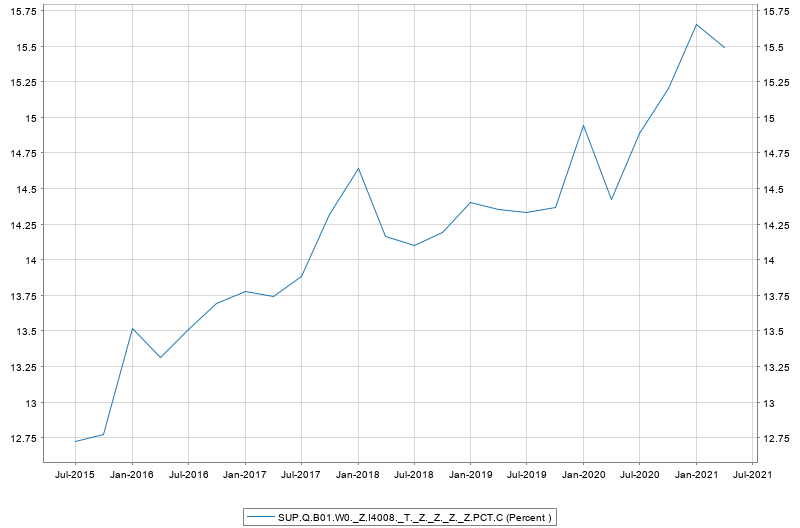

The exciting, and unnoticed inflection point for European banks is that the multi-year battle to increase capital is over. The average Tier 1 ratio across Europe is now over 15%. Banks are now well capitalized and prepared to grow again.

Another big change thanks to the coronavirus pandemic is that the political emphasis has shifted from using monetary policy to prevent a financial crisis to instead using monetary policy to cultivate REAL economic growth. Both politicians and regulators acknowledge banks are much stronger than in 2007 and Europe needs banks to lend to grow economically.

The tone has changed. Banks are no longer seen as evil, & instead the new view is the economy needs banks to lend to small businesses, and finance the ‘Net Zero’ climate transformation, which is a big theme in Europe. Thanks to these changes European bank assets began growing in 2020. The trend is accelerating and bank assets are now well over 40 trillion.

The Capital Return Trend

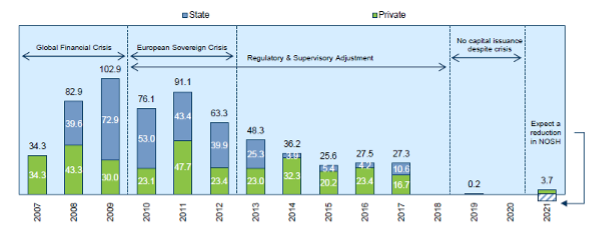

Europe’s highly capitalized banks can grow again, but they are also able to increase dividends and buy back shares. After over a decade of capital raises and bailouts the banking sector share count is starting to decrease. This is a big inflection point.

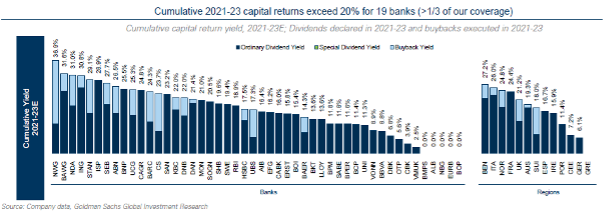

Many banks in Europe will return over 20% of their market cap in dividends and share buy backs from 2021 to 2023. That’s 20% just from capital returns without any growth or revaluation.

Despite this key inflection point in the sector’s leverage ratios, many banks are trading at a discount to the European stock market.

Earnings revisions trends are already starting to trend more & more positive, and with the recent ECB decision in October to raise rates 0.75%, we’ll see even more upgrades. Euro banks might be the new energy or coal mining sector.

European banks are the most highly capitalized they’ve ever been, so their improved earnings will :

A. Flow into new loans, and

B. Get distributed as dividends and share buybacks.

Both of which benefit you, the shareholder.

Also, look at the chart below of bank earnings sensitivity to .25% rate hikes. Last month they JUST announced .75%, and now imagine what happens if they announce another 150-200bps of rates hikes next year.

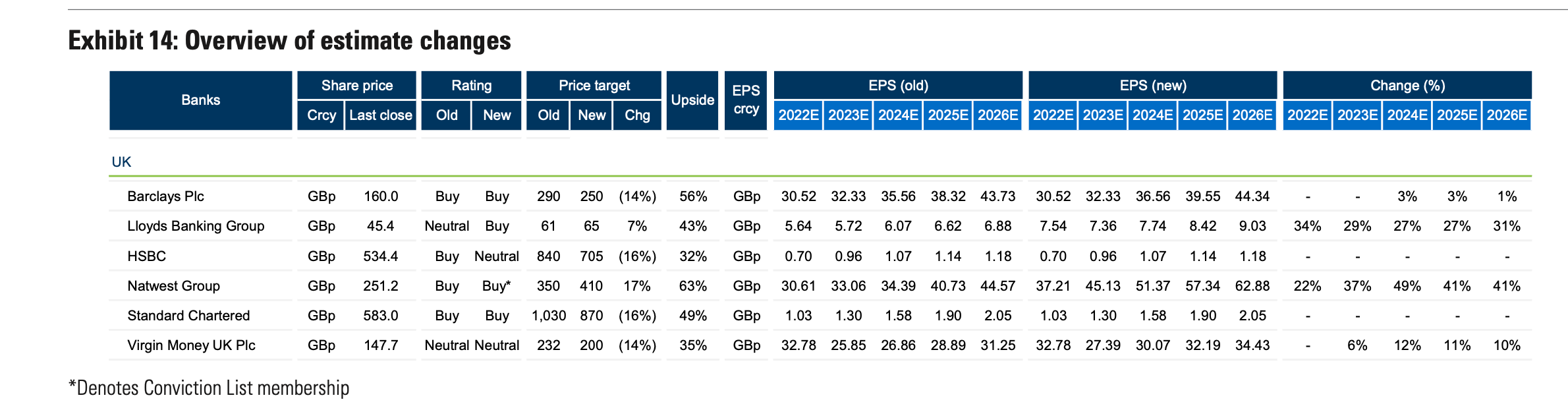

Finally, look at the earnings estimate changes coming through for Natwest and Lloyds. 30-40%+ increases? What other sector is getting 30% estimate increases in 4Q2022?

The stocks on my shopping list include Commerzbank, Amrobank, Natwest, AIB Group, and the European Bank ETF ( EUFN 0.00%↑ )